Inflationary or deflationary?

The AI boom is both. Or possibly neither

Home Office officials are not paid to be cheerful. Perhaps that is why for decades, every new secretary of state received the same bleak assessment: that crime would continue on its inexorable rise. And the logic, it seemed, was unimpeachable.

During periods of economic recession, where there is more poverty and higher unemployment, there is greater incentive for illegal activity. Meanwhile, during periods of economic growth, there are more consumer goods in circulation, and so greater opportunity for theft.

Indeed, this played out in the data. Crime had increased, largely uninterrupted, for half a century following the end of the Second World War. It rose during the ‘never had it so good’ 1950s and the swinging sixties, the three-day weeks of the 1970s and mass unemployment of the 1980s.

And then, around about the mid-1990s, crime began to fall — not just in Britain but in other high-income countries too. And no one really agrees on why. Explanations range from the reduction in lead exposure to more liberal abortion laws, better car and home security to ageing societies, greater use of CCTV by police and later the shift to online commerce1.

The unsettling thing isn’t that the forecasters were wrong — it’s good that crime fell! Rather, it’s that when all roads appear to lead to the same destination, that’s usually an indication the map is somewhat askew.

High on their own supply shocks

Earlier this week, the head of Northern Trust’s $1.4 trillion asset management unit predicted that advances in artificial intelligence had “the potential to be massively disinflationary”, thanks to widespread efficiency gains. Mike Hunstad told the Financial Times:

If even a portion of those actually materialise on an economy-wide basis, it could be one of the biggest positive supply shocks we’ve ever seen… You can’t ignore that.

We’re all accustomed these days to negative supply shocks — those sudden decreases in the economy’s productive capacity. They occur when something bad has happened: think the Covid-19 pandemic, Russia’s full-scale invasion of Ukraine or the closure of the Strait of Hormuz. Basically, supply falls, prices rise.

Positive supply shocks, on the other hand, occur when there is a sudden increase in an economy’s productive capacity. Something has made it cheaper to produce goods and services, and as a result prices tend to fall (or rise more slowly). Think China’s accession to the World Trade Organisation, the US shale oil boom or the dramatic reduction in the costs of solar and wind power.

There appear to be three broad responses to the AI boom. The first from the boosters, often with a financial interest, who believe the technology will transform whole swathes of cognitive tasks, reshaping (or destroying) jobs, how value is created, wars are fought. Then there are the doubters, who argue that AI is overhyped, its many products loss-making and the industry is driven as much by bored venture capitalists as by any real productivity gains.

Finally, there are the people whose eyes simply roll to the back of their heads whenever the subject is raised. I’m firmly in the latter camp, but when the subject turns to AI’s impact on inflation, I begin to take an interest.

Productivity puzzle: solved?

Alright, so we have advances in AI leading to a seismic rise in the supply of goods and services, driving prices lower. This, Hunstad argues, will allow the US Federal Reserve to reduce interest rates2 without stoking inflation, much as the flood of cheap Chinese consumer goods in the mid-2000s enabled central banks around the world to keep borrowing costs low amid an era of robust economic growth.

Hunstad is far from alone. Writing for the International Monetary Fund, economist and Nobel laureate Michael Spence observed:

AI is our best chance at relaxing the supply-side constraints that have contributed to slowing growth, new inflationary pressures, rising costs of capital, fiscal distress and declining fiscal space, and challenges in meeting sustainability goals.

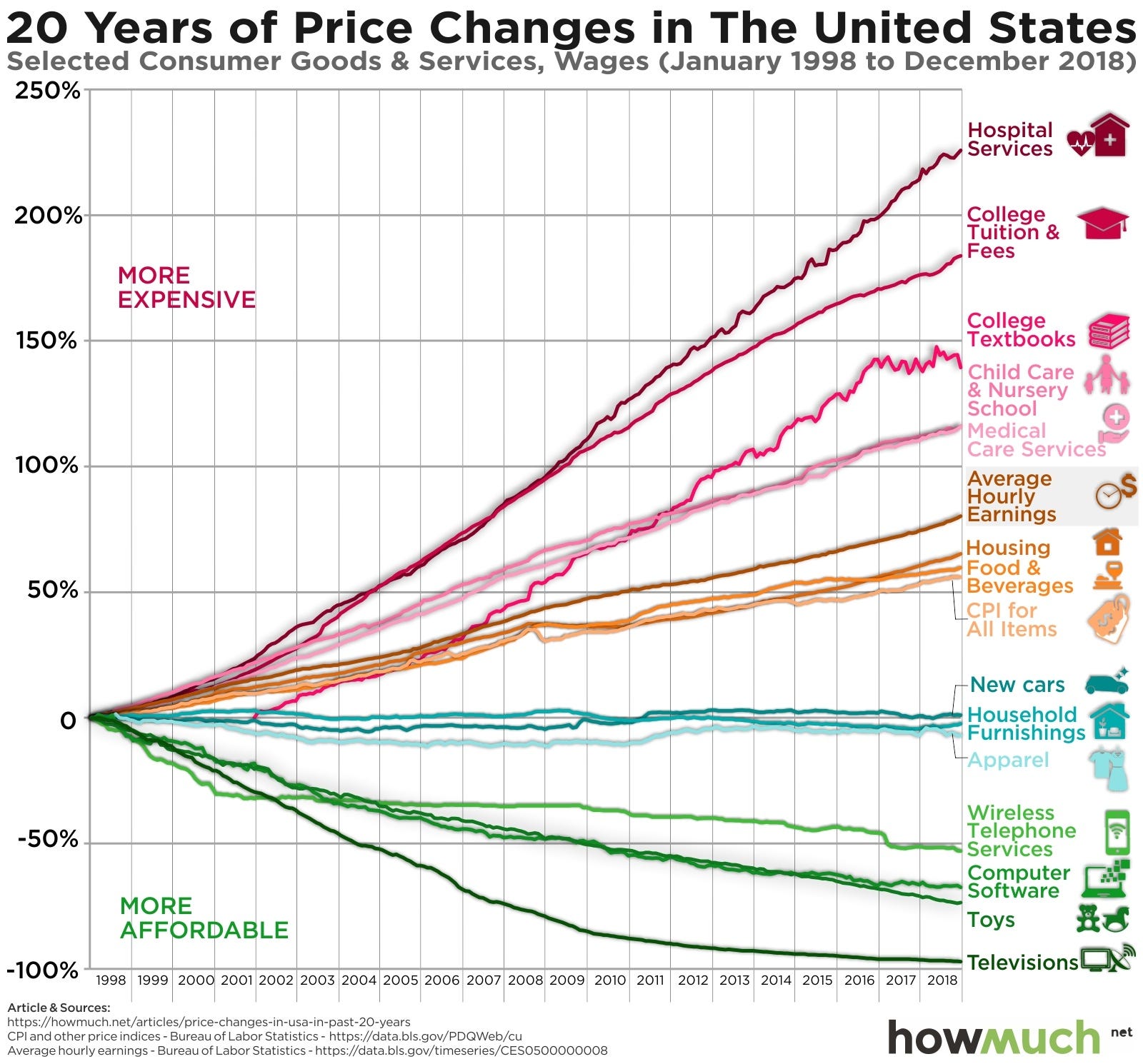

You want numbers? Well, a 2025 study in Economic Letters found that “AI diffusion is associated with reduced inflationary pressures,” with a 10–percentage-point increase in the share of firms employing AI corresponding, on average, to a 0.3–0.6 percentage-point decline in inflation, with a particularly pronounced impact in the dominant services sector.

But there are a few reasons to be sceptical. First, the sheer amount of investment in AI infrastructure, in data centres, energy infrastructure, high-end chips and indeed high-end talent, risks raising prices in the short-term, when any productivity gains of AI are likely to take longer to materialise.

In other words, even if AI is itself deflationary — building AI is inflationary. Earlier this year Andrew Sheets, a strategist at Morgan Stanley, told Reuters that US consumer price inflation would remain above the Fed’s 2% target3 until the end of 2027 “in part because of heavy corporate investment in AI.”

Then there is our friend, Baumol.

Pepto-Baumol

Ok, very briefly because I already burned through 250 words at the top on crime forecasts that was parenthetical at best to my thesis. Baumol’s cost disease (a name so cheery it could have been drafted by Home Office officials) is the idea that in labour-intensive, low-productivity sectors (such as education and the arts) wage increases tend to match those in more productive sectors (such as manufacturing).

The classic example is that of a string quartet. It takes as many musicians the same amount of time to perform a Schubert piece today as it did in the 19th century. Yet the real wages of those pesky violinists have risen substantially over the last hundred years. And those costs are borne by higher prices for concertgoers.

So here’s an added wrinkle on AI and prices. Should the most optimistic of the AI boosters be right, and productivity growth goes through the roof. Administrative work is completed in the blink of an eye and abundance is everywhere. What used to take a week of tedious data inputting is now completed by AI in half an hour. Well, won’t that make Baumol’s cost disease even more acute?

Those violinists, teachers, nurses — anyone left behind in the inherently human, low-productive sectors, whose output cannot be scaled with AI — will still demand to be paid more, propelled by the productivity bonanza all around them. What will that do to the price level?

These roles may also be among the safest in the economy — AI can support teachers or plumbers, but it is unlikely to replace them. Worse still, many of these lower productivity sectors provide essential services, often paid for in full or in part by already cash-strapped governments.

Of course, like those old Home Office civil servants, these predictions could be wrong, right or right for the wrong reasons. For instance, should AI lead to mass unemployment precipitating a near-total collapse in aggregate demand, you might still get deflation, but the bad kind, the end of times variety, rather than the cheap-Chinese-manufactured-T-shirts-on-sale-in-Zara-supply-expansion kind.

Which is just as well. I’ve long believed that Deflationary Spiral would be an ace name for a glam rock band.

Where, of course, a lot of the crime has shifted

Won’t somebody please think of the asset prices!

This was pre-Iran War

This is the kind of analysis that is urgently required. However my I interest here is, erm, more fundamental, dare I say, and without minimising your newsletter today.

Simply, can liberal democracy as we have known it, survive a full implementation of AI potentialities? I think that means activities and consequences not yet know. This should be, in a way, exciting to think about, but I am not really excited. Why? Fear of the unknown or unknowable?

What I do know that, in essence, it’s all about control of one’s.life, community, country…

I’ll leave it there as this is not a political sociology seminar!

Jack, a late, light-hearted question: have you ever tried to trick ChatGPT with what you thought was a good trick question? Like which of four things is the odd one out?

I did recently and no chance. Below just for interest:

Which is the odd one out?:

Isthmus of Suez

Isthmus of Panama

Isthmus of Kra

Isthmus of Corinth

It answered correctly that this related to canals and that Kra doesn’t (yet) have one dissecting it.

Is it possible, even in theory?