The Iran energy shock is bad

But it's not Ukraine bad (yet)

Another exogenous supply shock, another energy crisis, another round of inflation with the usual course of central bank tightening. Here we go again. But before the parallels with 2022 petrify into received wisdom, and whether you sit on the Monetary Policy Committee or not, it is worth pausing. Because the latest supply shock differs in some important ways from the last one.

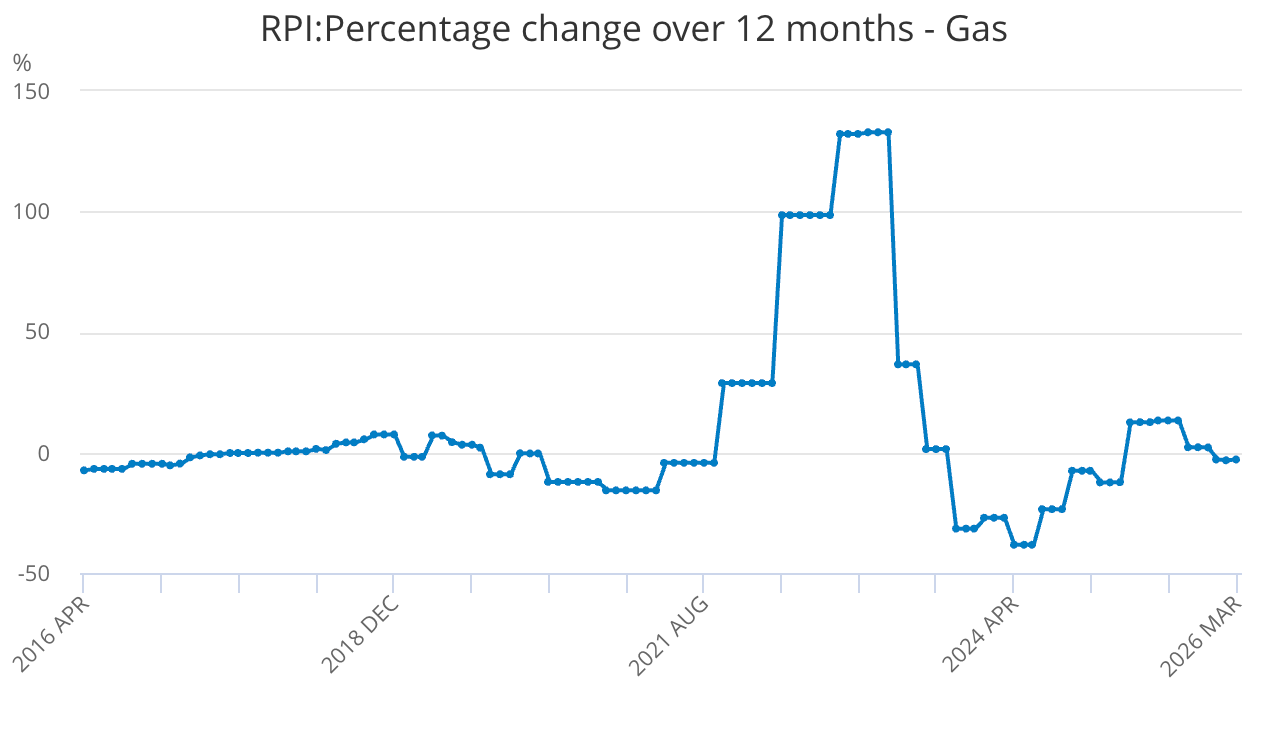

The energy crisis Britain faces is — thus far at least — smaller than the one which followed Vladimir Putin’s full-scale invasion of Ukraine. In the aftermath of the February 2022 Russian offensive, UK gas prices peaked at 300p per therm above pre-war levels. Compare that to 78p today.

This feeds into household energy costs. But for the Energy Price Guarantee, the typical household bill would have hit £3,549, a rise of 80%. Compare that to today, where forecasts for the July energy price cap have jumped to £1,973. Painful, and a 20% rise compared with April, but not yet on the same level.

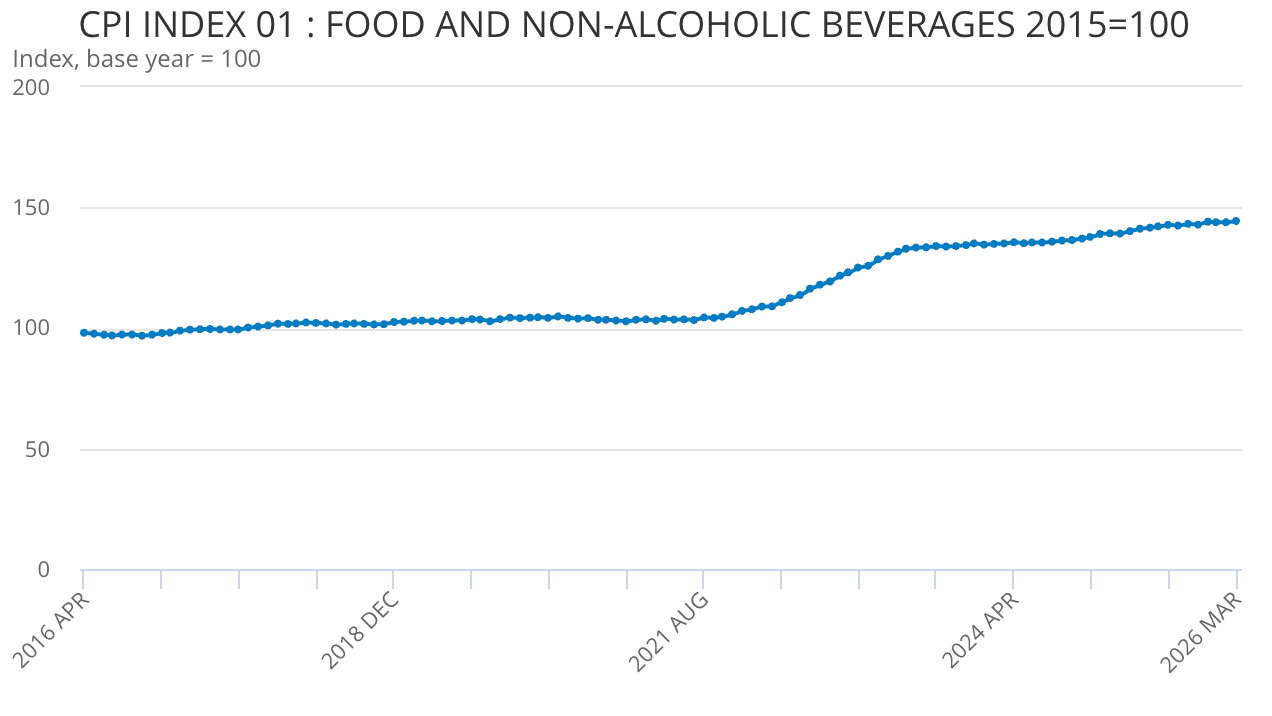

Then there is food, which saw a year-on-year increase of 19.1% in March 2023, the highest rate since 1977. In fact, over the three years between May 2021 and May 2024, food prices rose by a stomach-churning 30.6%, according to the House of Commons Library. Compare that to today, where the Food & Drink Federation expects a “gradual but persistent pickup in food inflation”, reaching 9-10% by the end of the year.

Next, we come to the broader economic environment. The war in Ukraine coincided with a post-Covid re-opening of the British and global economy. All those supply chain bottlenecks would have been broadly inflationary even without Vladimir Putin’s adventurism. Recall there were major shortages in all manner of materials, such as plastic, concrete, steel and timber. The cost of shipping spiked dramatically too. In January 2021, it cost a mere $1,500 to send a shipping container from Asia to Europe. A year later, that figure had jumped to $17,000.

Little wonder that the Bank of England’s February 2022 Monetary Policy Report, published prior to the Russian invasion, forecast CPI inflation peaking at around 7.25% in April 2022. Compare that to today. Prior to the US-Israeli military action against Iran, the Bank forecast inflation would fall to 2.1% in early 2026.

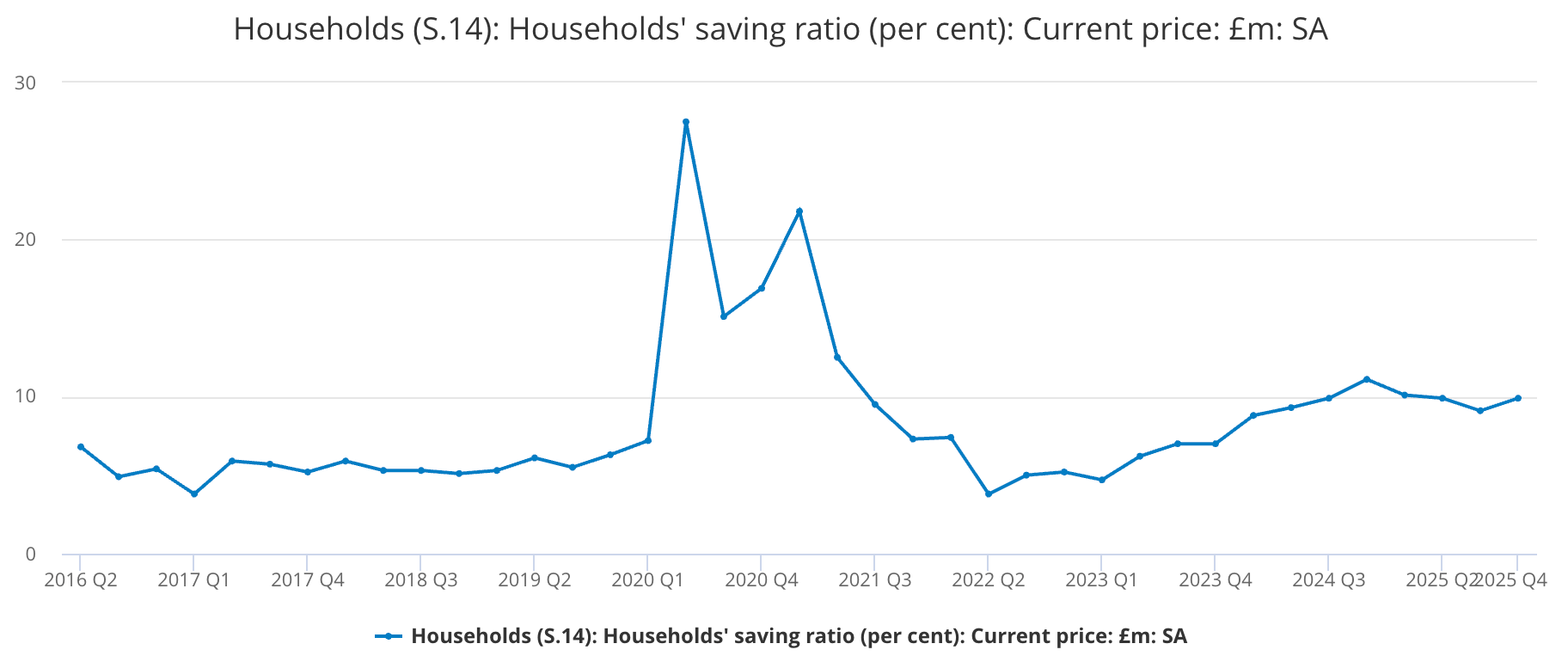

Moving on to the demand side, there were numerous other inflationary pressures. Consumer demand back then was strong — during the pandemic, the UK savings ratio hit a thirty-year high. Hardly surprising given that people weren’t allowed to leave their homes. This spare cash, in concert with those supply chain problems, was inherently inflationary.

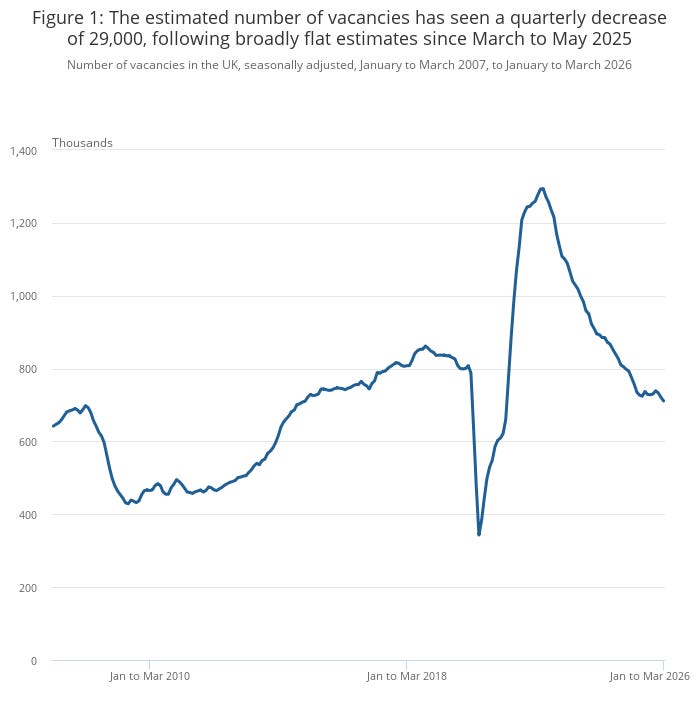

Now, consider labour. Post-pandemic, the jobs market was extremely tight, with total vacancies peaking at almost 1.3 million in February to April 2022 and growth in private sector earnings peaking at 8.1%. Compare that to today, when the labour market is soggy, vacancies have fallen to 711,000 and private sector pay is less than half the post-Covid peak. All in, businesses simply have far weaker pricing power.

It is also worth a brief glance at consumer sentiment which is, frankly, on the floor. GfK’s Consumer Confidence Index, which measures a range of attitudes on households’ financial expectations and views on making major purchases — fell to -25 in April. As for business confidence, April’s CBI Industrial Trends Survey hit -20%, meaning more thought output would decrease than increase over the next three months, compared with 0% in March.

Apologies for a newsletter groaning under the weight of statistics. If a politician were to deliver a speech of this sort, I’d be the first to suggest that it was a poor use of time and paper. Moreover, I really don’t intend to suggest that the Iran war is no biggie. For one thing, those Bank of England rate cuts for later this year — also known as the government’s growth strategy — have been flung far out of the window.

And that’s before we consider the impact on the global economy, the energy transition, food security, the freedom of navigation, the US as hegemon, the Labour government’s re-election chances, terrorism against Jews, the bond markets, Gulf nations, the semiconductor supply chain — it is massive and, until the Strait of Hormuz reopens, still very much ongoing. The comparison with 2022 may well become apposite.

My point is only: this is a supply shock hitting a largely disinflationary backdrop, not an inflationary one. Even if that doesn’t make the pain to come any less real.

Jack, there is such detail here that it almost requires textual analysis. (Fear not!)

The data on UK gas prices (300p per therm v 78p today) suggests a problematic market for consumers. Many are the reasons, I suppose, why energy prices have not dropped to (somewhat) mirror this drop. If they have, who perceived it?

I’m not sure I can see the data points on the ONS Gas chart which would explain the 20% rise we can expect and which you reference.

I think it is not too controversial to say that the calculus of decision making on interest rates depends on when the current crisis ends. The media drone on that for a few weeks, the shocks might be containable, ie don’t panic. But these weeks are now extending into months. Interest rate cuts previously pencilled in are now academic. There is now a probability relationship between the time it takes to settle this crisis and the amount of interest rate increases we see over a 12-month time horizon.