What happens when America stops borrowing

Record US deficits are a global problem. Then again, so were its surpluses

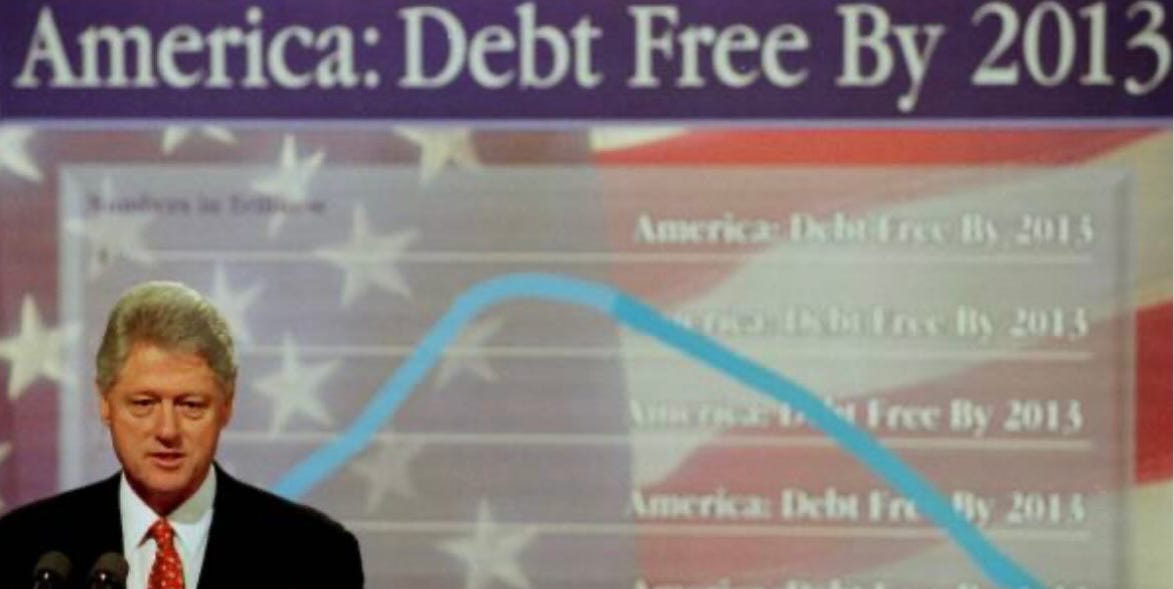

It was among the best economies in living memory. In 2000, the United States was nine years into what was then its longest peacetime expansion1. Unemployment was low, inflation moderate and the stock market at historic highs. But there was a problem, indeed a potentially systemic risk. Not the dot-com bubble or the packaging of sub-prime loans into mortgage-backed securities, but US borrowing. Specifically, the lack of it.

The federal government ran a budget surplus of $236 billion in fiscal year 2000, roughly 2.4% of GDP. This was driven by a confluence of economic and political forces: a booming economy, surging tax revenues (particularly capital gains) and the deficit reduction policies of first the George H. W. Bush and then Bill Clinton administrations.

So America had won the Cold War, its economy was going gangbusters and the New York Yankees defeated the Mets to secure the World Series. What was the issue again?

Check your privilege

The world needs dollars. Central banks hold them to stabilise their currencies and backstop their financial systems. Governments use them to participate in international trade and meet foreign debt obligations. Businesses require them because commodities, most notably oil, as well as many major international contracts are priced in dollars, even if neither party is American.

As a result, all of these want to hold vast reserves of dollars, mostly in the form of US Treasury bonds. This acts as a financial safety net and facilitates trade. What this means in practice is that the US benefits from being able to:

Borrow at lower rates than it otherwise could

Run larger trade deficits without precipitating a currency crisis

Be the flight to safety during global crises (even ones it causes)

Impose financial sanctions on foreign governments, given how much global commerce touches the dollar system

Little wonder that former French President Valéry Giscard d'Estaing called America’s reserve currency status the ‘exorbitant privilege’. And boy have Americans been enjoying it.

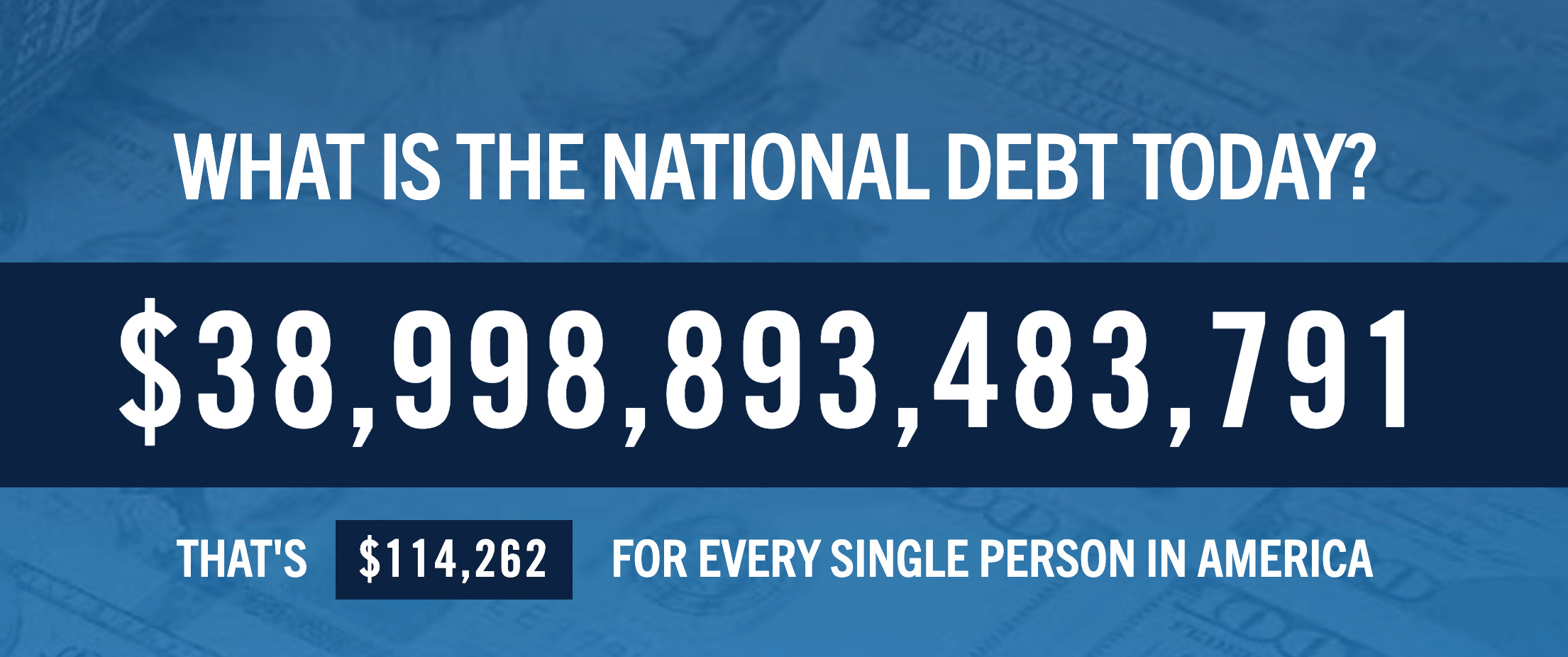

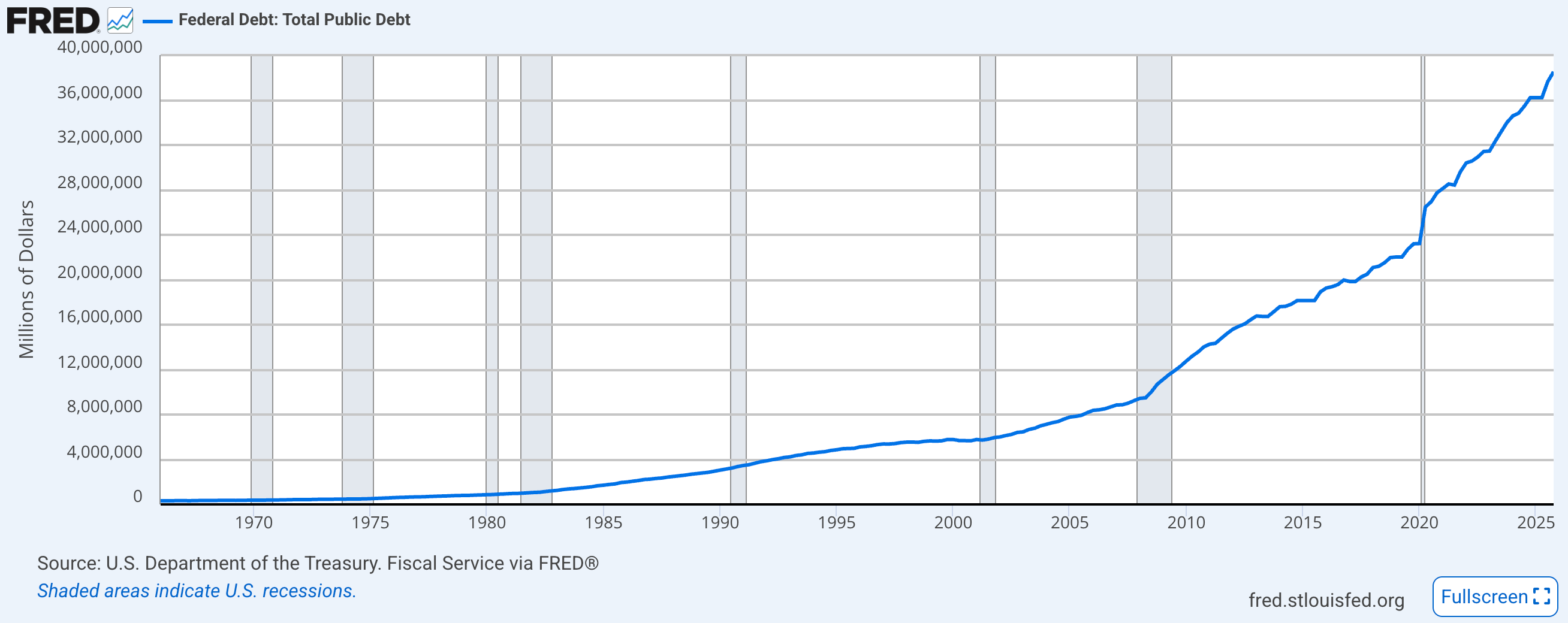

Today, US debt stands at approximately $39 trillion or 124% of GDP. And it continues to grow. Even prior to the Iran War, the federal deficit stood at around $2 trillion, up from $1.8 trillion the year before, and the year before that, and the year before that.

And this isn’t the ‘good’ or ‘necessary’ sort of deficits that occur during recessions. These are structural and happening amid a period of economic expansion — when debt as a proportion of GDP is supposed to fall. So to put Giscard d'Estaing in blunter terms: the rest of the world is financing America’s appalling fiscal behaviour.

"Our currency, your problem”

This is indeed a problem, both for the US and the rest of the world. For the former, there is:

The threat of higher long-term interest rates as the government has to compete with private borrowers for available capital

Reduced fiscal flexibility as interest repayment costs crowd out other spending

Further political dysfunction e.g. debt ceiling standoffs

Generational inequity — current spending is effectively financed by future taxpayers

For the latter:

The risk to creditor nations — either in the form of a US default or, more likely, attempts to inflate away the debt burden, reducing the real value of foreign dollar holdings

The spillover effects of Federal Reserve policy — higher US interest rates to control inflation draw capital flows towards US assets, which raises borrowing costs globally

Erosion of confidence in the dollar system

Right, so that’s now several hundred words spent on the problems of unsustainably high US debt in a newsletter that promised to be about the systemic risk of low US borrowing. Which is where we now turn.

Quantity has a quality of its own

Why doesn’t Denmark provide the global reserve currency? It’s got the perfect economy (it sells both Lurpak and Ozempic), strong political institutions and is a pretty open economy. The answer is simple: Denmark’s economy is way too small and so lacks the scale of issuance to meet global demand. Because even if the Krone were the greatest asset imaginable: accepted by all, safer than gold, helps you to lose weight — there simply aren’t enough in circulation.

Denmark is set to borrow just 109 billion krone this year or roughly $12 billion. That’s not nearly enough currency to facilitate Indian oil purchases or Brazilian soybean exports. America got to be the global reserve currency because it has the largest economy. But the sheer size of its debt in fact generates the liquidity in the market for… US debt. If there weren’t enough of the stuff, the trade in it (and therefore global trade in general) could grind to a halt.

And this was the threat, at least in theory, back in 2000. If the US budget was in surplus, it wouldn’t have to issue quite so much new debt. And if it didn’t need to issue new debt, the market for US Treasuries would become less liquid. And if foreign countries couldn’t get hold of US Treasuries, what would that mean for the dollar’s status as the global reserve currency?

It gets worse (or, at least, nerdier). So I’ll let Lloyd Blankfein, former chief executive of Goldman Sachs, explain:

The Treasury market also provides the curve against which corporate bonds and the credit of other governments are priced. If the US began paying down the national debt, what would credit spreads spread from?

In other words, everything else — corporate bonds, mortgage rates, emerging market debt — is essentially priced as “Treasuries plus X basis point”. If President Al Gore had meaningfully paid down US debt, what would have replaced the benchmark?

Mo Money Mo Problems

As we know, this issue never came to pass. One moment, the Congressional Budget Office was projecting surpluses from sea to shining sea, the next came the dot com crash and related 2001 recession, the George W. Bush tax cuts, the post-9/11 spending binge and the Global Financial Crisis.

I share this story in part because I’ve been reading Blankfein’s terrific memoirs (can you tell?) but also, I just really like it. Not America’s collapse into distressed borrower status and political demagoguery, but the concept that, in economics, good things are bad and also bad things are bad. I suppose it validates the curmudgeon in me.

Further evidence that 1-0 to The Arsenal is indeed the perfect result.

Eclipsed only by the June 2009 to February 2020 expansion (128 months), spectacularly ended by the Covid-19 pandemic.

Congrats! Raise a glass to the team of the year. Since Arteta can now be compared to “the Professor”, he can draw some measure of satisfaction….

What I’m wondering is whether the board will go all “Abramovich”(I think you know what I mean), and send him packing…..

The US debt & deficits levels are always expressed as “federal”. If a federation is the sum total of the constituent states, is it worth asking which group of states most contribute to the overall figure? I mean I have never heard of the total budgetary position of the US being the sum of the federal & all the state budgets. Am I making any sense?